Black Friday 1869 is a revealing historical subject because it opens a clear path into the people, events, and wider changes that shaped its era.

On September 24, 1869, the American gold market lurched into panic, brokerage houses cracked under the pressure, and a day that would become known as Black Friday exposed just how brittle the nation’s post–Civil War financial system really was. The drama centered on two of the era’s most notorious speculators, Jay Gould and Jim Fisk, who believed they could control the price of gold and profit from the resulting scramble. Instead, their scheme collided with the power of the federal Treasury, a volatile currency system, and a public that already distrusted Wall Street’s growing influence. The result was more than a spectacular market failure. It was a national lesson in how speculative ambition, weak oversight, and political uncertainty could combine to shake confidence in the young industrial economy.

To understand why the episode mattered so much, it helps to remember that the United States in the late 1860s was still living with the monetary aftershocks of the Civil War. Paper money, greenbacks, National Bank notes, and gold all circulated in a confusing system in which prices could move sharply and trust was never guaranteed. Gold was not merely another commodity. It was a benchmark for trade, a reference point for international commerce, and a symbol of stability in an economy still trying to recover from wartime finance. When Gould and Fisk tried to corner it, they were not just gaming a market. They were probing the seams of the entire financial order.

Black Friday 1869 remains a vivid case study in Economic History because it shows how much damage a handful of well-connected actors could do in a thin, information-poor market. It also reveals the limits of federal authority at a time when the government was still learning how to manage modern finance. The panic that followed struck brokers, merchants, farmers, and exporters in different ways, but its effects were broad and lasting. The episode became a warning about market concentration, insider access, and the dangerous illusion that clever speculators could outmaneuver the public interest.

The Civil War Money System and Why Gold Mattered So Much

The years after the Civil War were financially unsettled because the United States had not returned to a single, simple currency. Wartime spending had produced greenbacks, or United States notes, which were not fully backed by gold or silver. They were legal tender, but their value fluctuated against specie. At the same time, the government had developed a more complex national banking structure, and the older habit of treating gold as the ultimate measure of value had never disappeared. In everyday life, this meant that Americans were often thinking in two different monetary languages at once: paper currency for domestic circulation and gold for the deeper world of finance and foreign trade.

Gold mattered because it anchored confidence. Importers needed it to pay for goods abroad. Exporters watched its price because a rising gold premium could make American products cheaper in foreign markets. Investors used gold quotations as a shorthand for the health of the economy. If the gold price rose relative to greenbacks, it signaled that paper money was losing ground. That made gold a political as well as financial object. Debates over whether to expand, restrain, or eventually redeem paper money in specie were tied to broader conflicts over debt, inflation, and the burdens of reconstruction.

This was also a period when financial information traveled unevenly. Telegraphs made prices more visible than before, but the market was still susceptible to rumor, manipulation, and delays in transmission. That combination created opportunities for those with money, connections, and nerve. The marketplace was not yet governed by the kind of disclosure rules and regulatory institutions later generations would take for granted. If you want a broader sense of how speculative enthusiasm could overrun reality in the nineteenth century, the Poyais Affair is a striking reminder that fraud and imagination often flourished where oversight was weak.

In this environment, gold was unusually powerful because it was both a commodity and a signal. Its price could be pushed upward through concentrated buying, but only if the market believed the rise would continue. That belief was exactly what Gould and Fisk hoped to manufacture. Their project took advantage of the era’s monetary uncertainty, betting that if enough gold could be removed from circulation, panic would do the rest.

How Jay Gould and Jim Fisk Tried to Corner the Gold Market

Jay Gould and Jim Fisk were unlikely partners in style but effective collaborators in speculation. Gould was quiet, calculating, and deeply strategic. Fisk was flamboyant, theatrical, and eager for public attention. Together, they operated through the Erie Railroad and a network of allies, and they began to see gold not just as a financial asset but as a lever that could be pulled for massive gain. Their plan was straightforward in concept even if complicated in execution: buy as much available gold as possible, restrict supply, drive the price higher, and profit from the surge.

To make the scheme work, they needed more than buying power. They needed time and political cover. If the federal Treasury sold gold into the market too aggressively, the corner would collapse. So Gould and Fisk worked to influence policymakers and cultivate intermediaries who might either block Treasury sales or at least provide warning before action was taken. Their efforts exploited a murky line between legitimate market participation and political manipulation. In an era when personal access often mattered as much as formal rules, that line could be quite profitable.

The mechanics of the corner depended on creating scarcity. By accumulating large quantities of gold, the conspirators hoped to force traders to borrow at increasingly high rates to cover their positions. As prices rose, panic buying could intensify the squeeze. The plan also relied on psychological pressure. If market participants believed gold was truly scarce, they would rush to protect themselves, pushing the price even higher. The scheme thus depended not only on the amount of gold controlled but on the collective emotions of the market.

Yet the whole enterprise had an obvious weakness: the U.S. Treasury still held enormous power over the gold supply. Gould and Fisk tried to neutralize that power through influence and timing, but they could not control every decision inside the federal government. Their attempt also revealed an uncomfortable truth about nineteenth-century finance: speculative markets could be distorted by actors who knew how to exploit gaps between public institutions and private ambition. In that sense, Black Friday was not simply the story of a failed corner. It was the story of how easily market confidence could be undermined when a few insiders tried to bend the rules for private advantage.

Grant’s Intervention and the Moment the Scheme Broke

The turning point came when President Ulysses S. Grant decided the government had to act. As gold prices climbed and speculation spread, Treasury officials became alarmed that the market was being manipulated. The Treasury began releasing gold, and that decision shattered the speculative logic behind the corner. Once it became clear that federal gold would enter circulation, the scarcity Gould and Fisk had tried to engineer could no longer be sustained. Traders who had bought in hopes of a continued rise suddenly found themselves exposed.

This intervention mattered because it showed that the federal government still possessed a crucial stabilizing role, even if its actions were reactive rather than systematic. Grant’s decision reflected a concern not just for market integrity but for public order. If the gold market spiraled out of control, the damage could spread far beyond the trading floor. Prices, contracts, and credit relationships were all vulnerable. In a period when the financial system was still closely tied to the real economy, a sudden shock in the gold market could quickly become a broader economic emergency.

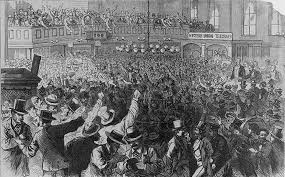

When the bubble burst, the impact was immediate. Gold prices plunged, brokers scrambled, and many who had speculated on the basis of continued increases were trapped. Some traders had borrowed heavily to join the rally. Others had sold short, expecting the bubble to break. The collapse created winners and losers in a matter of hours, but the scale of disruption was much larger than any simple tally of gains and losses could capture. The episode showed how the mechanics of a corner could become a social crisis once confidence evaporated.

Importantly, the collapse did not merely embarrass Gould and Fisk; it exposed the uneven power structure of the financial world they inhabited. They had access to money, influence, and information, but even they could not fully override the state’s capacity to intervene. At the same time, the need for such intervention revealed how underdeveloped financial safeguards still were. The government had to react to a private market crisis in real time, without the benefit of modern circuit breakers, transparency rules, or a central bank capable of smoothing the shock. Black Friday was a reminder that markets can be both powerful and fragile, especially when institutions lag behind speculation.

The Panic’s Effects on Brokers, Farmers, Exporters, and Public Trust

The immediate pain of Black Friday fell first on brokers and speculators, but the consequences did not stop there. Brokerage houses faced extreme stress as margin calls hit and positions collapsed. Traders who had borrowed money to buy gold or related securities found themselves unable to meet obligations. In a market built on confidence and credit, the speed of the reversal was devastating. The panic exposed how tightly interconnected the financial system already was, even in the 1860s.

Farmers and exporters felt the shock in less direct but still meaningful ways. A rising gold price had made some American goods more competitive abroad by lowering their relative cost in foreign-currency terms. When gold crashed, that advantage changed. Exporters had to recalibrate quickly, and those tied to overseas commerce faced uncertainty in pricing and settlement. Farmers, especially those already burdened by debt, were not insulated from the turbulence either. In the postwar economy, credit conditions mattered enormously, and any disruption in financial markets could tighten lending or worsen regional anxiety.

Perhaps more significant than the immediate economic damage was the blow to public trust. Gould and Fisk were already infamous, but Black Friday made them symbols of reckless speculation and the social power of Wall Street. Many Americans saw the episode as proof that financial elites could manipulate markets while ordinary people absorbed the consequences. That suspicion was not unique to 1869. It belonged to a broader nineteenth-century anxiety about the moral legitimacy of modern capitalism, an anxiety that also animated other notorious schemes and speculative bubbles in history.

The public reaction also reflected a deeper concern about government itself. Some critics wondered whether federal officials had been too close to the speculators; others believed the Treasury had acted too late. Either way, confidence in the fairness of the system suffered. Economic history is often shaped as much by trust as by balance sheets, and Black Friday showed how quickly trust could erode when people believed the rules had been bent behind closed doors. The scandal became a lasting cautionary tale about the dangers of opacity, insider access, and unstable monetary institutions.

What Black Friday 1869 Revealed About Regulation and the Future of Finance

Black Friday did not immediately lead to a fully regulated financial market, but it helped shape the long conversation that eventually produced one. The episode made clear that markets left entirely to private power could be manipulated in ways that harmed the broader economy. It also showed that government intervention, while necessary, could itself be limited by poor information and political entanglement. The challenge for later generations would be to build institutions that could reduce both manipulation and panic without freezing commerce altogether.

In that sense, the failed gold corner foreshadowed many later debates in American economic life. Questions about transparency, market concentration, insider trading, and the public role of the state did not begin in the twentieth century. They were already present in 1869, though framed in the language of specie, greenbacks, and railroad barons. The Black Friday crisis demonstrated that financial systems can be technically sophisticated and still profoundly unstable if oversight is weak and incentives are misaligned.

The story also helps explain why modern financial history remains fascinated by speculative episodes. Like other notorious schemes in the nineteenth century, the Gould-Fisk affair depended on asymmetry: they knew more, moved faster, and had better access than most participants. But no scheme can remain stable forever if it relies on the illusion that one group can command a market that is, in reality, shaped by thousands of competing decisions. Once the Treasury acted, the illusion collapsed.

Looking back, Black Friday 1869 was more than a colorful scandal involving two famous manipulators. It was a stress test for postwar American capitalism, and it revealed multiple vulnerabilities at once: an unstable monetary system, thin regulatory protections, political influence over market outcomes, and a public deeply sensitive to signs of elite abuse. That is why the episode still matters. It was not simply a failure of greed. It was a moment when the fragility of the entire financial structure became impossible to ignore.

In the end, Gould and Fisk did not master the market. They exposed it. Their failed corner showed that post–Civil War finance was already modern enough to be dangerous, but not yet modern enough to be safe. The lesson was painful, widely felt, and historically important: when money, politics, and speculation collide in an underregulated system, the damage extends far beyond the traders who made the bet.

Related reading: The Great Hedge of India: the British Empire’s forgotten living customs barrier, The Poyais Affair: the fake Central American country that fooled investors and settlers.